Affiliated Manager’s Group (AMG) Financial Analysis

Affiliated Managers Group, also known as AMG, is “an American international investment management company that owns stakes in a number of boutique asset management, hedge fund, and specialized private equity firms,” according to WikiPedia. By the end of 2016, AMG’s managed assets were self-reported at “approximately $727 billion”.

From Google Finance

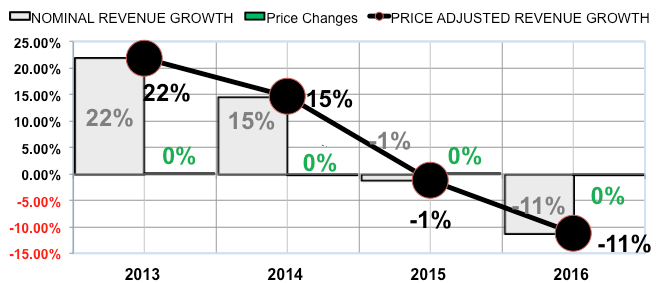

1 – Real Revenue Growth

AMG is made up of numerous firms that were bought up or merged together. Revenues started declining precipitously in 2015 after robust revenue growth rates in the prior 4 year (an average of 17% annually). The stock market dropped and so did the revenue growth of Affiliated Managers Group.

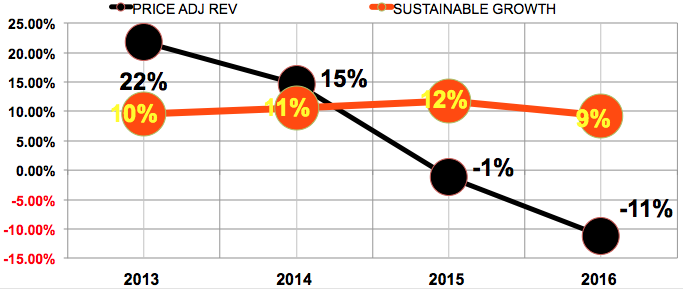

2 – Sustainable Revenue Growth

Since 2011 the firm has not had sustainable revenue growth. In other words, the company grew revenues faster than the balance sheet could support them. It wasn’t until the last two years of revenue decline that it is now sustainable. It is interesting to note that 94% of the revenue growth that occurred from 2011 through 2014 was due primarily to the stock market increase.

More on sustainable revenue growth »

3 – Pricing Policy

It is assumed that out of all expenses 25% of revenues is allocated from operating expenses to the direct expenses for all the relationship managers to deal with the clients. Since this is not outlined specifically in the financials it has to be assumed. This means that the pricing policy would be neutral in this analysis.

4 – Operating Expense Control

Operating expenses have been well controlled and growing half as fast as the revenue growth. In 2012, the operating expenses to revenues were 53% and by 2016 they stand at 42% to revenues.

More on operating expense control »

5 – EBITDA to Actual Cash Flow

Actual cash flows are sporadic and often anemic. These cash flows could be stronger and more consistent if the company was not frequently buying or merging with other firms within its industry. That raises another question, addressed below.

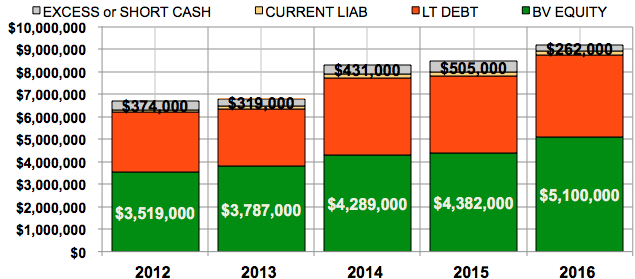

6 – Debt Free Cash Flow

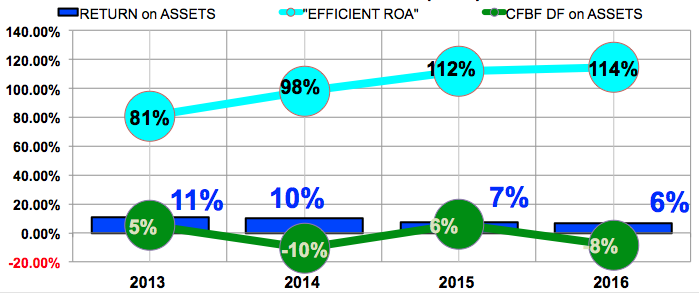

Over the period of this analysis – 2012 to 2016 – revenue growth has been approximately 5% a year, while asset growth has been around 12% a year. Total liabilities, however, have grown at 13% a year, which is just not sustainable.

Even just looking at the assets growing near the debt level, I’m skeptical about the quality of those assets being purchased. Most of these assets are in Other Assets, which shows the purchase of other companies in the booking of goodwill. But over the same period of time, the rate of return on assets has declined from 11% to 6%. I hope that this type of investing is not the same philosophy used with their clients.

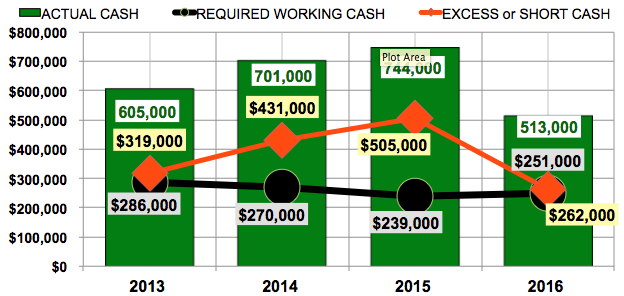

7 – Excess Cash

Excess cash is a difficult concept to discuss with business owners and investors. Holding excess cash does not necessarily make a business financially secure, nor is it a good idea to do just from a prudence viewpoint. Similar to holding excess accounts receivable balances or increased inventory balances or excess fixed assets, it lowers your rate of return and increases your costs capital. Excess cash is a lazy asset that doesn’t earn much.

Almost 80%, $400 million of AMG’s cash assets of 500 million, is excess. They must be holding onto that money to make those wonderful investments we talked about above!

8 – Return on Assets

As mentioned above, the return on assets (ROA) is declining and falling under the actual cost of capital, the cost to put money to work in their business. As of March 31, 2017, the implied investors’ required cost of capital to invest in the stock was around 9.33% and the company’s 2016 ROA was only 6%.

More on return on assets (ROA) »

9 – Working Capital Needs

Each year the company covers its working capital needs without a problem (all that excess cash makes this hard to screw up).

10 – Debt Financing

The company has a book equity of around 58% to total assets. It still has room to borrow more capital; the question is whether it should given the comments above.

More on use of debt financing »

11 – Net Trade Cycle

Managing annual working capital for companies like this shouldn’t be that difficult as the variables are fairly consistent for the most part. The firm knows when and how much money it will collect in fees both monthly and quarterly. The firm can also control to some degree when it pays out monies for operational expenses.

AMG, however, has a spread in its net trade cycle of 12 days – from a low of 35 to a high of 47. Each one of those days is the equivalent of around $6 million, adding up to $72 million sloshing around back and forth in the working capital of the company.

This means that the company can swing from a gain in the net trade cycle from $72 million to up to a loss of cash flow of $72 million. There’s no reason for this and it typically is representative of bad financial management.

12 – Cost of Capital and EVA

Given that the internal companies cost of capital is only averaging between 6 to 7% annually, it’s hard to believe that the last two years it cannot hurdle or exceed that rate. It is not achieving the required rate of return, hence the stock is lower than it could be.

For company like AMG, one that touts its ability to help outside investors invest their money, it is strange to see these kinds of financial inconsistencies along with an apparent inability to manage their own money.