Coach, Inc Financial Analysis: Room for Improvement

Coach, Inc. is a luxury goods manufacturer based out of New York that started as a family business hand-making wallets and billfolds in 1941 and has grown into a $5 billion global mega-brand over the last few decades. Coach was sold by the family to Sara Lee in 1985 and went public as Coach, Inc. in 2000.

The stock price chart below (from Google Finance, COH) shows the roller-coaster this stock has been in the last 10 years. In our analysis below, we’re going to concentrate on the last 4 years or so and see what went wrong and what corrections we recommend.

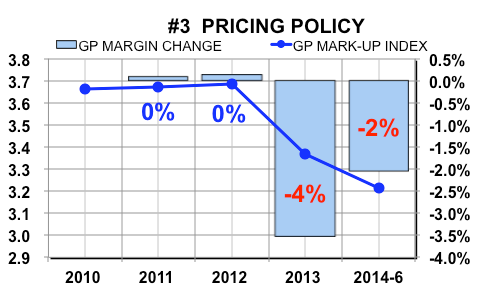

Pricing Policy

A strong brand like Coach should be able to maintain its gross profit margin at all times. People pay more for brand recognition, that’s been true for as long as we’ve had luxury consumer goods to purchase. Traditionally, Coach has done well with this but in 2013 and the the first half of 2014 the gross profit margins dropped significantly. This is unfortunate and the first thing that a company like Coach can and should fix but this has yet to happen. In fiscal year 2012, Coach’s gross profit margin was 72.8% but now is at 68.9% a decline of 5.4% and a cost of almost $200,000,000 for the fiscal year 2015 ending in June.

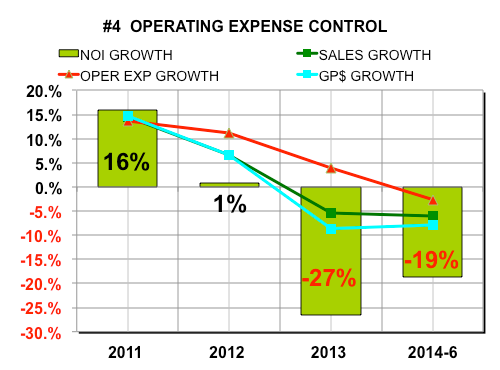

Operating Expense Control

Overall, annual revenues for Coach are increasing at a paltry 2% but the costs of goods sold and the operating expenses are both increasing at around 6% annually. This causes net operating income growth to fall off. First, the company needs to raise its prices around 6% across the board in aggregate to fix the gross profit margin,then they need to tackle the operating expenses. This does not necessarily mean cutting workforce; even holding the line on increases for the next year would be a real benefit, although difficult to accomplish. Why cause further turmoil cutting trained, experienced employees that you need in the future?

Excess Cash

Coach holds too much cash and other assets that are inefficient and costly. Coach holds up to $1 billion in excess cash, which is not necessary for the working capital operations of the business. A line of credit or even one third this amount could be held for working capital operations if the company wants to be fiscally conservative.

The company also holds around $1 billion of other assets that are financially unnecessary for the operation of the business. Excess cash and other assets drive up the costs of capital and lowers the rate of return on assets (where excess cash and other assets reside). Coach has a costly and straightforward problem that can be addressed for a very positive overall outcome. This is Coach, afterall!

EBITDA to Actual Cash Flow

Coach does, fundamentally, know how to manage its balance sheet to maintain its cash flow before financing. With a stumble in 2013 the company has maintained its cash flow at around $850 million per year. Excellent control and financial management and all the reason more to wonder why the Coach is having the issues we identified above. That said, this is also the reason we believe that the company can handle and change these issues soon to the company’s benefit.

2 comments

Can we avail your free sample offer of your service?

What information do you need to provide same, we have audited reports since Y2009.

Due to the rules and environment we operate, our company name and analysis results cannot be made public and we need an ethical guarantee from your company that this will be the case.

As we are operating a small, currently loss making company, we will require your good services where related costs of your services need to reflect this.

Thank you

Allen

Executive Board Member

Alan,

Sorry for the delay here. Best way to contact us for an analysis is through our contact form here:

https://thebusinessferret.com/contact/

I saw your email come through a few days ago, let me know if you haven’t gotten a response to that yet.

And, just for the record, we NEVER publish analysis data from companies we work with. The analyses posted on this site are either fictional data or financial information pulled from SEC filings. Your confidentiality is extremely important to us.

Comments are closed.