Domino’s Pizza Financial Analysis

Domino’s Pizza (DPZ) has been in the news recently as they continue “a winning streak” with strong first-quarter earnings in 2015. They’re also exploring technological solutions to winning the crowded fast food market with Uber-style pizza delivery tracking for smartphones and a pizza design service called Pizza Mogul that lets people create pizzas and earn money for sales. These kind of creative and unique digital strategies have helped push Domino’s to record-level earnings and share prices.

But even the most creative companies need to manage their finances in a way that will keep them growing and experimenting with new sales strategies. We wanted to see if the numbers behind this fast food giant support all the great financial press we’ve seen lately.

We were not disappointed.

Domino’s Pizza Pricing Policy

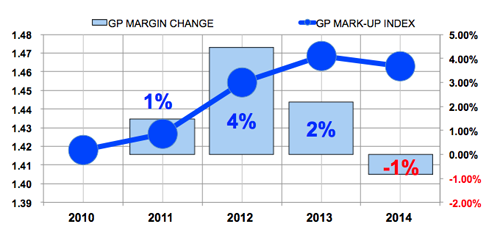

Domino’s Pizza is characterized by financial pundits as a highly profitable company in the fast food industry and we agree. Domino’s is one of the most profitable firms we’ve seen. Their stellar performance is largely due to the firm’s courage to raise prices even when revenues were declining in 2012. Even when revenues began to rise, the company continued to raise prices prices. You can see in 2014 the price increases stopped and, unsurprisingly, the cash flow growth slowed in turn. Keep the cash flowing, Domino’s!

EBITDA for Domino’s

Net income goes up and so does cash flow. Domino’s works to keep the revenue growth rate in line with working capital needs hence increasing cash flows. This is the kind of chart we like to see for all companies, regardless of industry.

Take a second to compare this chart with the pricing policy one above. From 2011 to 2014, GP markup (a function of pricing) went up overall, as did sales growth. Many businesses are fearful of raising prices because they see their customers fleeing to cheaper options. Even in a highly competitive industry with minimal differentiation, Domino’s increased their GP margin while enjoying higher sales. The perfect combination!

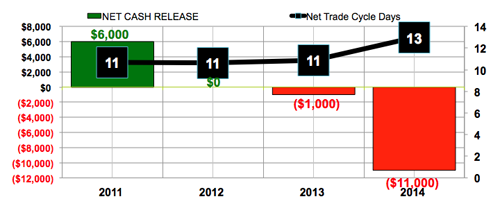

Domino’s Pizza Net Trade Cycle

With the exception of 2014, the company has kept their working capital needs to a manageable 11 net trade cycle days. This means that the company turns their cash cycle in 11 days. The more stable this relationship is the more the company can successfully plan revenue increases while still producing solid cash flow.

The two day bump in net trade cycle days in 2014 means that the company needed to invest $11,000,000 back into the working capital cycle, eating up cash and cash flow. Eat pizza, Domino’s, not your cash flow. You know better!

1 comment

I’d like to make the suggestion that if Domino’s was able to raise their prices and see improved revenue it must be due to inelastic demand for their pizza. They must have had a consultant, or someone in-house, review their books and calculate their elasticity of demand before making the decision to raise prices. In essence, though raising their prices would inevitably reduce number of sales they found a price which minimized losses and maximized revenue. It’s an incredibly effective business strategy that often goes overlooked due to it’s counter-intuitiveness.

Comments are closed.