Granite Construction Financial Analysis

According to their website, Granite Construction is a “builder of roads, tunnels, bridges, airports and other infrastructure” operating out of Watsonville, California. They’re known for their work on Interstate 64 in St. Louis, the Queens Bored Tunnel in New York, and the Las Vegas Monorail, the 3 combined topping $1B. This company is building big things.

While never a great measure of good financial practices, their stock price has seen better days. It spiked to almost $74 in 2007 but fell dramatically right after and has stayed generally flat around $35 ever since.

But we’re not here to talk about the stock price, we’re here to show what’s behind the financial management.

Granite Construction Revenue

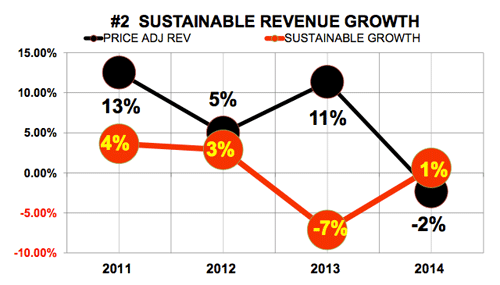

For Granite Construction the revenue picture is all over the map – up and down year-by-year but generally downward. This is a picture of a company who goes after any and all revenue channels to hit a dollar target.

This kind of wild fluctuation might be excusable in a less stable industry but, with the economy improving as it has been, a company building infrastructure should be setting and hitting clear targets year over year. Granite’s annual revenue rollercoaster shows there is something amiss.

Here, we see revenue sustainability based on price adjusted revenue growth generally unsustainable throughout this period with wide variations. variations. This contributes even more to an apparently uncontrollable financial situation.

Erratic, unsustainable annual revenues are typical of construction companies – both big and small – resulting in similar and ongoing financial issues consistently sees in this industry.

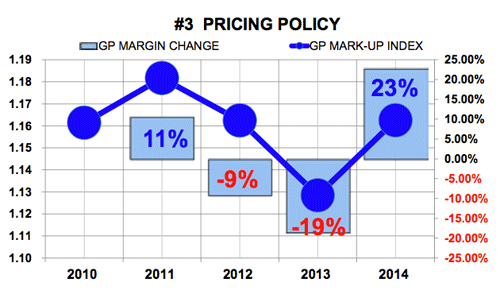

Granite Construction Pricing Policy

With declining revenues, the company is forced into a pricing policy that appears totally reactive and random. Instead of introducing better finance strategies, Granite is reacting year after year with pricing changes that threaten to throw them even further off the track.

EBITDA to Cash Flow

The net result of this wild variation is cash flow crashing from an already low amount relative to revenues, then going negative. This negative cash flow adds to the unsustainability of annual revenue growth, making matters worse. It is also increasing net trade days, constraining cash flow even further.

It does not have to be this way but we’ve seen many construction companies run into this same dangerous financial scenario. Our recommendation? Stabilize the revenues, fix the pricing policy, and then work on the working capital issue. Your business depends on it.