The Middleby Corporation Financial Analysis

The Middleby Corporation (MIDD) is “an American publicly traded commercial and residential cooking and industrial process equipment company based in Elgin, Illinois” (Wikipedia).

From Google Finance

Pricing Policy

Middleby Corp is considered by the financial commentators as a real dedicated cash flow generator. One might question this by looking at the pricing policy. A real cash flow generator does not allow the markup index and, as a result, the gross profit margin to decline continuously for several years!

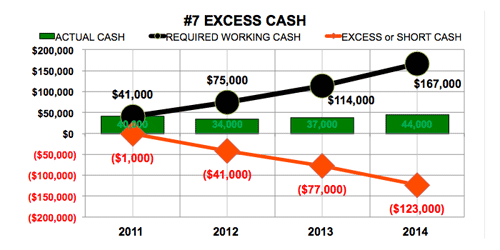

Excess Cash

Holding cash does not make a company a cash flow generator but generating enough cash flow that you have no need for working capital cash absolutely is. Well, that is not the case with Middleby. Actual cash is stable but the working capital cash need is rising directly in lock step with the negative excess cash.

EBITDA to Actual Cash Flow

Considering just these last two charts and looking at the actual annual cash flow generation in the third chart prove this point.

For the most part, actual cash flow and adjusted cash flow on a debt free basis is basically flat until 2014. During the years prior the annual nominal revenue growth is around 23% but the cash flow is flat and actual non-adjusted cash flow is mostly negative due to investments into other assets.

While investments into other assets may be declared necessary to grow the business these rapid investments need to be growing the cash flows and they are not doing so. In fact, the fixed assets investments directly related to the business was in half from 2013 pace compared to 2014 boosting cash flow and the pace of investing in other assets was cut back further adding to the jump in adjusted cash flow for 2014 yet actual cash flow before financing was still negative.